The transition from cash-based to digital payment environments presents both opportunities and challenges for venue operators across diverse industries. Custom prepaid card programs offer sophisticated solutions that maintain operational efficiency while serving customers who prefer or require alternatives to traditional payment methods.

The transition from cash-based to digital payment environments presents both opportunities and challenges for venue operators across diverse industries. Custom prepaid card programs offer sophisticated solutions that maintain operational efficiency while serving customers who prefer or require alternatives to traditional payment methods.

This guide examines the business case, implementation framework, and optimization strategies for prepaid card programs that deliver measurable value to both operators and customers.

The Strategic Business Case for Prepaid Programs

Prepaid card programs provide value that extends well beyond simple payment processing. They support operational efficiency, improve customer experience, and generate strategic business intelligence that can reshape decision-making.

The most immediate benefit comes from operational cost reduction. Traditional cash handling requires staff for counting, reconciliation, deposits, and change management—introducing human error and security risks. Prepaid systems eliminate much of this overhead while also reducing theft and shrinkage.

Prepaid programs also improve transaction speed. Cash exchanges slow lines during peak periods, while prepaid transactions process in seconds. Faster throughput increases venue capacity without additional staffing, directly supporting revenue growth and customer satisfaction.

Finally, prepaid programs unlock data analytics. Unlike cash, every prepaid transaction is traceable, generating insights into customer preferences, spending behavior, and visit frequency. These insights support better inventory planning, pricing strategies, and targeted marketing campaigns.

Program Architecture and Design Considerations

Design decisions made at the outset of a prepaid program determine its long-term success. These include architecture type, account structure, card technology, and system integration.

One of the first choices is between closed-loop and open-loop architectures. Closed-loop programs limit usage to specific venues or networks, giving operators full control and simplified compliance. Open-loop programs allow broader acceptance but introduce additional regulatory complexity.

Account structures vary as well. Single-use cards require minimal infrastructure but limit engagement, while reloadable cards encourage repeat use and reduce per-transaction costs. Hybrid approaches support both use cases.

Card technology influences functionality and security. Magnetic stripe cards are inexpensive but less secure, while chip-based and dual-interface cards offer enhanced fraud protection and future readiness.

Finally, integration architecture determines whether the system operates standalone or connects with POS, inventory, or CRM platforms. Integrated systems unlock richer data and greater efficiency.

Card Design and Branding Strategy

Physical card design is more than a technical detail—it is a brand extension. Colors, typography, and graphics should reinforce brand identity while remaining legible and durable.

Security elements such as holograms, microprinting, and color-shifting inks deter fraud while communicating trust. Many venues also deploy limited-edition or collectible cards tied to events or promotions to increase engagement and retention.

Technology Infrastructure and System Integration

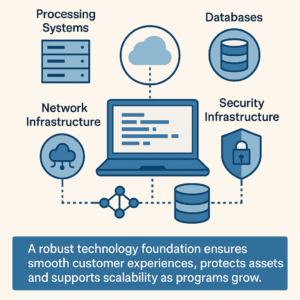

Reliable infrastructure underpins every prepaid program. At the core, processing systems manage account creation, balance tracking, and transaction authorization.

Reliable infrastructure underpins every prepaid program. At the core, processing systems manage account creation, balance tracking, and transaction authorization.

Databases must be protected through encryption, redundancy, and backups, while network infrastructure connects terminals, kiosks, and administrative systems with redundancy and offline safeguards.

Security infrastructure—including access controls, intrusion detection, and continuous monitoring—protects financial and personal data while supporting scalability.

Customer Acquisition and Program Launch

A strong launch strategy drives adoption. Preparation begins with staff training, followed by multi-channel marketing and promotions such as bonus value on first loads.

Many operators begin with a soft launch to refine messaging and identify system issues before a full rollout. Once stable, high-visibility launch events can accelerate adoption.

Promotional Strategies and Customer Incentives

Prepaid card programs thrive on continuous engagement. Incentives may target acquisition, usage, reloads, or partnerships, sustaining engagement while increasing lifetime customer value.

Operational Management and Customer Service

Operational excellence includes secure balance management, dispute resolution, and card inventory tracking. Versatile systems streamline operations across venue types.

Customer service should support balance inquiries, lost card replacement, and transaction disputes through multiple channels, ensuring accessibility and trust.

Financial Management and Accounting

Funds loaded onto prepaid cards are recorded as prepaid liabilities until redeemed. Regular reconciliation ensures accuracy.

Unused balances (breakage) may be recognized as revenue depending on regulations. Transparent fee structures and conservative accounting policies protect compliance and customer confidence.

Data Analytics and Business Intelligence

Data Analytics and Business Intelligence

Prepaid transactions generate insights unavailable with cash. Segmentation, predictive analytics, and lifetime value modeling support smarter pricing, inventory, and engagement strategies.

Regulatory Compliance and Legal Considerations

Prepaid programs must comply with consumer protection laws, escheatment rules, PCI DSS requirements, and data privacy regulations. Proactive compliance protects both brand reputation and customer trust.

Mobile Integration and Digital Innovation

Mobile apps, digital wallets, QR codes, and push notifications extend prepaid program functionality while improving convenience and engagement.

Program Evolution and Continuous Improvement

Continuous improvement through feedback, benchmarking, and technology upgrades ensures long-term relevance and performance.

Strategic Partnership Opportunities

Co-branded cards, loyalty integrations, retail distribution, and technology partnerships expand reach and differentiate prepaid programs.

Conclusion

Custom prepaid card programs reduce costs, accelerate transactions, enhance customer experience, and generate valuable business intelligence.

Custom prepaid card programs reduce costs, accelerate transactions, enhance customer experience, and generate valuable business intelligence.

By asking the right questions early, designing thoughtful architecture, and maintaining operational excellence, operators can create programs that deliver long-term value.

As payment ecosystems evolve, prepaid programs remain flexible platforms that adapt to new technologies—serving as a competitive advantage in digital-first environments.

Custom Prepaid Card Programs FAQ

What’s the typical implementation timeline?

Implementation typically takes 3–6 months depending on complexity, including integration, compliance review, card design, training, and pilot testing.

How do closed-loop and open-loop programs differ?

Closed-loop programs have fewer regulatory requirements but limited acceptance. Open-loop programs allow broader use but require compliance with payment networks and PCI standards.

What is typical breakage?

Breakage rates vary by industry and program design, commonly ranging from 5–20%.

Can prepaid programs integrate with loyalty systems?

Yes. Modern platforms support API integration with CRM and loyalty systems, enabling unified customer profiles and rewards.